Analysis: Is Lemonade losing its fizz?

Need to know

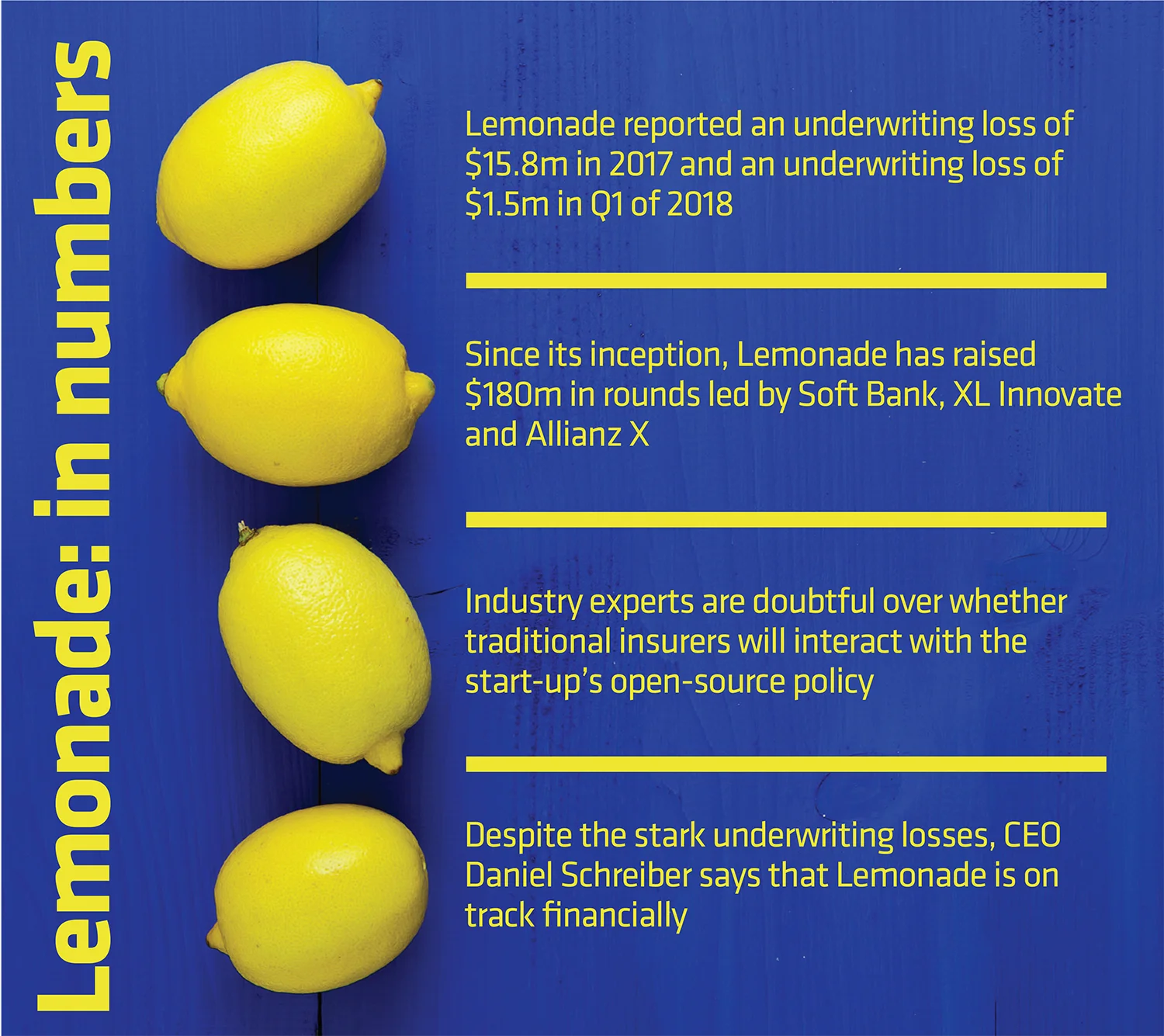

- Lemonade reported an underwriting loss of $15.8m in 2017 and an underwriting loss of $1.5m in Q1 of 2018

- Since its inception, Lemonade has raised $180m in rounds led by Soft Bank, XL Innovate and Allianz X

- Industry experts are doubtful over whether traditional insurers will interact with the start-up’s open-source policy

- Despite the stark underwriting losses, CEO Daniel Schreiber says that Lemonade is on track financially

Will Lemonade’s losses see its success go flat?

Seemingly every week, a new start-up promises to disrupt the market. These brave new insurtechs raise questions from industry veterans about what they do, how they plan to do it and why on earth they came up with that name.

Yet none have fuelled as much discussion and column inches as US-based insurtech Lemonade.

From its commitment to pay a claim in seconds, to its promises to reform the “word salad” of traditional insurance policies, Lemonade’s bold business model has attracted major investment from the likes of XL Innovate and Allianz X. But the company is suffering major losses, raising questions of whether its business model is sustainable in the long term.

Lemonade reported a total underwriting loss of $15.8m (£20.7m) in 2017 and a comparatively small new written premium of $8.3m worth of renters and home insurance. Already in the first three months of 2018, the start-up reported an underwriting loss of $1.5m.

Despite some rumblings across the industry over the numbers, its CEO Daniel Schreiber remains confident that the business is on track to be where it needs to be.

“Our sales last year were just shy of $10m. Our loss ratio is stabilising but remains too high,” Schreiber told Post.

“Those who say that our underwriting losses are unsustainable are guilty of stating the obvious. We have strategic reinsurance agreements, so our net losses have been at a healthy 60% and it is our partners who bear the brunt of those losses. These losses are unsustainable but the business model is not. The numbers are too small to reach any conclusion.

“We have planned for these results and things are going ahead as scheduled. Our underwriting losses are not worrying our investors, regulators or reinsurers. You cannot expect a start-up to have the data needed to get it spot on the first time around.

“Traditional insurance companies forget that tech companies like us take five to seven years to turn a profit. We’re just now reaching the point where the data is credible and, as we go on, we will see our loss ratio decline significantly.

“We are in continuous contact with our regulators and they acknowledge that you don’t draw long-term conclusions from short-term results. Our losses are not something that puts our business at risk.”

Infrastructure

Lemonade has built a lot of its own systems from scratch, including its underwriting and distribution systems. It means that it is shouldering a lot of the costs itself.

But Schreiber said that building the systems in this way also enables the company to make cost savings.

“There’s a lot of cost benefit to building our systems ourselves,” he said. “We did evaluate every system on the market before building our own and, by identifying fault in current systems, we do feel as though we add value to the market. Our systems are a lot more agile than those used in companies 100 times our size. This gives us full confidence that we are on the right track.”

Long game

Perhaps many in the industry are pessimistically expecting Lemonade to meet the same demise as insurtech peer-to-peer start-up Guevara. The start-up, backed by Mosaic Ventures, closed for business in September last year after it failed to make quick returns.

However, Nick Pester, partner at Plug and Play, said that Lemonade’s investors are playing a long game and the firm is operating in a less stringent regulator environment than its UK counterparts.

“We need to bear in mind that US investors are more liberal than in the UK, the valuation of losses works a lot differently,” said Pester.

“US businesses are valued at roughly 50% less in the UK market. Lemonade’s investors acknowledge that it’s a long game, unlike Guevara’s investors who had an ultimately short-term view. Lemonade’s investors aren’t expecting the business to break even and make a profit right away.”

However, Pester warns that Lemonade can’t be too lax when it comes to turning a profit and that the next two years should see the start-up bringing in significant cash flow.

“You do have to wonder how many funding rounds Lemonade can get before the loss ratio starts improving,” Pester said. “Its investors will have thought very carefully about year-on-year losses. There may be the possibility that those investors won’t take on other rounds if business doesn’t start booming. The next two years will be crucial for Lemonade; either it will begin turning a profit or lose big investors.”

Investors speak

Despite the losses, its investment stream has been fast flowing. Founded in 2015, Lemonade began its operations in 2016 and now has licence to operate in 28 states in the US; the company has raised $180m worth of financing so far from big names including Soft Bank, XL Innovate and Allianz X.

Some incumbents have regarded Lemonade with an air of scepticism, so it is interesting that some of its investors are big players in the insurance sector. Its trailblazing qualities make the start-up an attractive prospect for its insurer investors: Lemonade has the agility to do what most incumbents are struggling to do and this has prompted a lot of financial interest. Namely, its slick claims process and its rapid issuing of policies was something that sparked interest from Allianz X.

“Allianz fully supports Lemonade’s strategy and growth plans,” a spokesperson from Allianz X said.

“We are pleased with their ability to redefine insurance by implementing technology to make the process of issuing policies and handling claims as easy as possible, while giving back to their customers through efficient claim payments and allocations to charities. This is just the beginning for them and we understand that it takes time to transform a largely antiquated industry.”

Policy 2.0

The insurtech isn’t just gleaning investment from insurers, Lemonade has also beckoned traditional insurers to interact with its Policy 2.0. The new policy strays from the traditional insurance model; the wording has been shortened so as to be readable in 10 minutes and customers are able to increase and decrease their coverage as and when they please.

“From a consumer point of view, policy wording is incredibly problematic,” said Schreiber.

“The policy has gone up on Github, where open-source software is developed. We’ve seen a surprising amount of interaction with the policy and it has been heartening to see customers engaging in the policy. We would love to say that this will lead change in the industry, but we are sceptical as to whether or not insurers will interact with it.”

For some, what Lemonade is doing with Policy 2.0 should be celebrated as something which will help steer the industry towards the change it has so far struggled to achieve. However, Dan White, senior partner at Ninety Consulting, said that insurers aren’t yet sitting up to take note.

“Policy 2.0 smacks of trying to shift the traditional industry,” said White. “The policy is trying to reduce the number of exemptions, cut out a chunk of the wording and ultimately improve things for the customer. Millennials want to engage with their insurance – this allows them that option. They can update it as they please, rather than having to get a new quote and purchase a new policy.

“We have encouraged our clients to engage with the policy but we have found that traditional insurers aren’t interacting in a serious way. What may well happen is that traditional insurers take part of the policy and use it to replace large chunks of their own wording.”

Legacy

What Lemonade lacks in profit and a book of business fit to rival that of incumbents, it makes up for in agility. Nigel Walsh, partner at Deloitte, said: “The advantage of Lemonade being so new is that it doesn’t have a large legacy book.

“This means it has a long way to go in terms of customer acquisition and turning profits, but it is starting from a point which allows it to be agile in the digital age.

Traditional insurers are struggling with their legacy books and building coding and systems to help tackle the problem, whereas Lemonade doesn’t have this issue.

“Its business model is quite different with its ‘give back’ element. It isn’t geared towards making a profit quickly; its model is more about scaling and growing its customer base first. There is something to be said for Lemonade’s continuous growth across multiple states in the US and once it scales sufficiently, you should expect it in Europe or Asia.”

Lemonade’s ‘Transparency Chronicles’ will continue to be published, detailing the growth of the business – warts and all. Only time will tell if the insurtech’s losses do improve, as predicted by its CEO.

But as the posterchild for the insurtech movement, its success or failure will likely have ramifications for the entire industry.

Further reading

Only users who have a paid subscription or are part of a corporate subscription are able to print or copy content.

To access these options, along with all other subscription benefits, please contact info@postonline.co.uk or view our subscription options here: https://subscriptions.postonline.co.uk/subscribe

You are currently unable to print this content. Please contact info@postonline.co.uk to find out more.

You are currently unable to copy this content. Please contact info@postonline.co.uk to find out more.

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@postonline.co.uk

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@postonline.co.uk

More on Technology

How ChatGPT is shaking up general insurance

An update on the launch of Aviva’s ChatGPT-powered insurance app and a call to action from WaniWani, which built the world's first, feature in the latest Insurance Post Podcast.

UK insurance chiefs’ demand for AI tools driving M&A plans

More than a quarter of insurance company chief executives have said an appetite to boost their artificial intelligence toolkit is driving their acquisition plans, but some are struggling with resistance from staff, according to a new survey.

Long-standing insurtech CEO replaced in new expansion push

Previsico chief executive Jonathan Jackson has been replaced as the insurtech enters what it has described as its next phase of growth with its sights set on expanding in the UK, the US and beyond.

Aviva bets on ChatGPT becoming major sales channel

Aviva expects artificial intelligence-led distribution to become a “material” sales channel for the insurer within the medium-term after becoming the first major UK provider to launch a ChatGPT app.

Over a quarter of insurance buyers strongly against AI use

Just over a quarter of UK consumers are very resistant to artificial intelligence being used in the insurance sector, according to a new survey.

60 Seconds With… IPI’s Craig Farley

Craig Farley, artificial intelligence and customer experience strategist at IPI, shares his dream of going back to the age of the dinosaurs plus his ambition to tackle mountain climbing.

Guidewire’s InsurPitch crowns first joint winners

A ‘wallet studio’ firm and a company seeking to connect vertical SaaS platforms with providers were the first joint winners of Guidewire’s InsurPitch.

Beazley leaning on data-driven underwriting in soft market

Beazley is increasingly pushing a data-driven underwriting approach for SME cyber cover in order to maintain discipline in a soft market.