Nexus Group's Colin Thompson on the evolution of MGAs

Need to know

- The litmus test for any MGA is its ability to underwrite a profitable book of business

- MGAs can be more flexible and opportunistic

- The UK MGA is stepping away from its past as a mono-line niche product underwriter

- MGAs need to embrace insurtech to ensure they have an efficient platform and model

With more than 300 UK-based managing general agents underwriting roughly £5bn - circa 10% of the UK general insurance market - the MGA is already firmly established within the London market providing a key access point to local markets and the ability to penetrate new or emerging markets.

The litmus test for any MGA is its ability to underwrite a profitable book of business and deliver low combined ratios to its risk carriers. Driven by the model combining underwriting expertise, distribution capability and efficient running via embracing technology, MGAs are growing in importance and number.

Operating without the regulatory restrictions and capital requirements of the traditional underwriter, the MGA can be more flexible and opportunistic. Considering the economic and political outlook for 2017, this should stand the MGA in good stead.

Despite Theresa May's speech on the 17 January outlining her priorities ahead of Brexit negotiations and intentions to pull the UK out of the single market, uncertainty surrounds how this will manifest itself. The precise nature of the "bold and ambitious free trade agreement" and corresponding passporting rights to the single market and the degree of transitional implementation remain complete unknowns. European policy holders are believed to account for around 5% of Lloyd's revenue.

With justifiable fears of US protectionism in the wake of Donald Trump's inauguration, the rise of disruptive technology within the insurance industry and potentially far-reaching French and German elections on the horizon during 2017, the turbulence of 2016 seems destined to continue.

In relative terms, compared with the traditional underwriter, the MGA's general attributes and low-cost basis should enable it to be more adaptable to negative developments offering innovative solutions while grasping opportunities as they arise. This can already be seen through regular influxes of new MGAs arriving on the scene, increased MGA mergers and acquisitions activity, innovative products and new distribution channels.

Where next for the UK MGA?

The UK MGA is stepping away from its past as a mono-line niche product underwriter to becoming a multi-product, multi-class ‘virtual' insurance company. This includes providing the entire infrastructure you would associate with an insurance company, for example, claims handling, providing actuarial services, premium collection and issuing policy documents.

The only difference is the MGA's balance sheet and that it doesn't carry the underlying risk - both of which offer advantages as discussed above.

A likely next area of MGA evolution is in the M&A space with the sector currently ripe for consolidation. This also feeds into increased size and here the US MGA model provides the yardstick. There are several mammoth US MGAs underwriting over $1bn in premium, while the largest MGA in the UK, Dual, underwrites over $900m. Increased capacity puts the MGA in a stronger negotiating position while also providing economies of scale.

Another likely direction for the MGA to evolve into is by also sourcing reinsurance solutions for their own portfolios that their underwriting partners ultimately then purchase. This would mean the MGA has greater control over the coverage that the reinsurers offer and, therefore, arguably greater consistency going forward.

Finally, MGAs need to embrace insurtech to ensure they have an efficient platform and model in order to remain forward looking and relevant. Incorporating big data and automating processes where possible will be key.

The MGA of the future may well be a combination of the above. A 'virtual' insurance company, underwriting at greater capacity, offering a wider product range while embracing technological advancements to remain cost efficient and competitive.

Only users who have a paid subscription or are part of a corporate subscription are able to print or copy content.

To access these options, along with all other subscription benefits, please contact info@postonline.co.uk or view our subscription options here: https://subscriptions.postonline.co.uk/subscribe

You are currently unable to print this content. Please contact info@postonline.co.uk to find out more.

You are currently unable to copy this content. Please contact info@postonline.co.uk to find out more.

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@postonline.co.uk

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@postonline.co.uk

More on Broker

TimeTo: Reflect on the 2026 Biba Conference

Content Director’s View: This week a swathe of the UK general insurance sector decamped to Manchester for the annual British Insurance Brokers’ Association conference. Jonathan Swift reflects on some of the themes and talking points of the 2026 iteration.

Industry welcomes fresh Financial Services Bill

The insurance industry has reacted following the introduction of the Enhancing Financial Services Bill introduced in the King’s Speech yesterday (13 May.)

Throwback Thursday: Biba’s new rules and tidy commercial

Insurance Post’s Throwback Thursday steps back in time to May 1981 to remind you what was going on this week in insurance history when the British Insurance Brokers’ Association was changing designations and commercial combined was a hot new thing.

Brokers cannot afford to be too passive, price led or generic

The operationalisation of data is becoming more important in helping brokers and their clients make better decisions in an increasingly volatile world.

Brokers lose share as direct insurers tighten grip on aggregator business

Despite cutting prices twice as fast as direct insurers, brokers are losing the battle for customers on price comparison websites, according to research from Consumer Intelligence.

City minister outlines plans to cut regulatory burden

Speaking at the opening of the British Insurance Brokers’ Association conference, City minister Lucy Rigby outlined the UK government’s plans to ease the regulatory load.

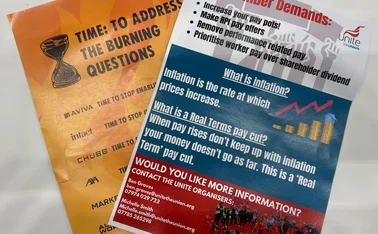

Climate and Union activists protest at Biba conference

Activists from both Extinction Rebellion Manchester and Unite the Union have staged protests at the British Insurance Brokers' Association Conference in Manchester.

Biba unveils cyber broker directory and ad campaign

The British Insurance Brokers’ Association has launched a national advertising campaign focused on cyber insurance alongside a specialist broker directory aimed at helping SMEs improve their resilience.